Global Analysis: Mapping Public Finance in the LNG Shipping Sector

Backed by global finance tracking databases, this analysis traces over USD $21.9 billion directed towards maritime LNG projects (76 deals involving public finance institutions and their subsidiaries that contributed to 62 maritime LNG projects).

Executive Summary

This study examines how public finance is contributing to maritime fossil Liquefied Natural Gas (LNG) projects globally. Public and commercial datasets were assessed to generate a database of deals involving public finance institutions contributing to maritime LNG projects. Methane, the primary component of LNG, is a short-lived, potent climate pollutant that contributes to a third of net warming since the Industrial Revolution. Reducing methane emissions is widely recognized as one of the most effective near-term strategies for keeping the 1.5°C temperature goal within reach. Understanding public finance flows to LNG projects is therefore critical for assessing alignment with global climate goals.

Key Findings

Despite climate commitments, public finance institutions continue to heavily fund LNG shipping, creating risks of stranded assets as the sector moves toward decarbonization.

Between 2013–2025, over USD 21.9 billion was directed towards maritime LNG projects (through 76 deals involving public finance institutions and their subsidiaries that contributed to 62 maritime LNG projects).

14 of these deals, worth over USD 8 billion, were labeled as “green” through broad, ambiguously defined green-finance frameworks and investment principles.

Over half of the USD 21.9 billion financing—upwards of USD 12 billion—was allocated specifically to LNG-fueled vessels and bunkering infrastructure. Public finance institutions played a major role in contributing to this financing through loans, credit guarantees, sale and leasebacks, and equity.

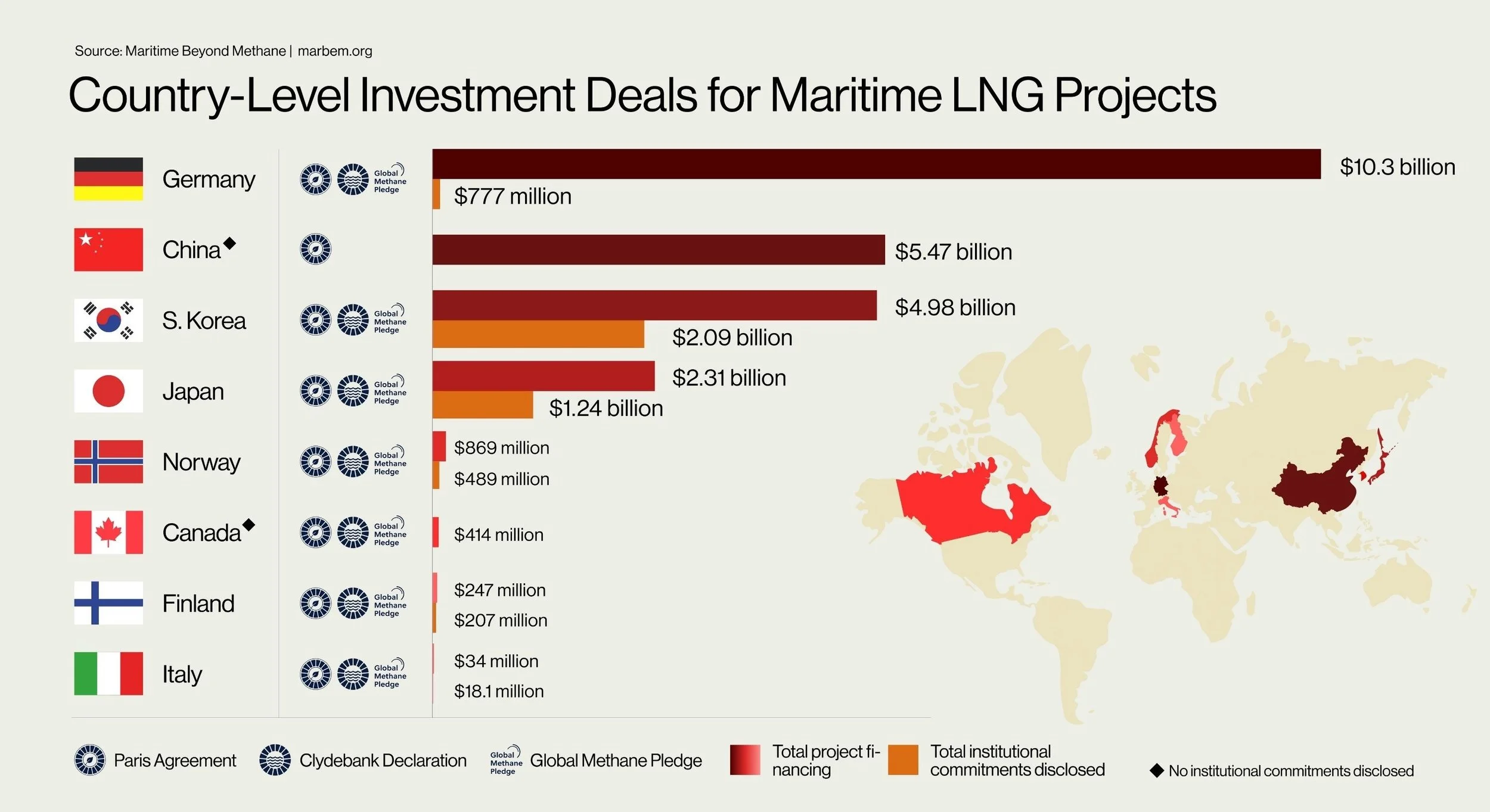

Public finance institutions and their associated private intermediaries from Japan, Germany, and China were top contributors to maritime LNG projects, despite commitments to the Paris Agreement and maritime decarbonization initiatives.

Many financial institutions obscure their involvement by restricting public reporting of information, channeling funds through private subsidiaries, or investing under “green” finance frameworks, enabling LNG investment to persist under the guise of sustainability.

There is an urgent need for greater transparency in shipping finance to address inconsistent financial reporting, the role of financial intermediary lending, and the role of sustainable or “green” finance frameworks in funding high-emission projects that will not be compliant with future decarbonisation policies.

Climate commitments and investment deals made by country, including total project fi nancing and total institutional commitments disclosed.

-

Bilateral Development Bank (BDB): Banks funded by a single country to support projects in partner nations

Credit: An arrangement where a lender (creditor) provides funds to a borrower (debtor) with the expectation of repayment at a later date, often with interest or fee

Equity: The value of ownership in a company or asset, representing the residual interest in the assets after all debts and liabilities are paid off

Export Credit Agency (ECA): Government-backed institutions that fund export projects

Floating LNG Vessel (FLNG): An offshore vessel designed to extract, process, liquefy, store, and offload natural gas at sea

Floating Storage Regasification Unit (FSRU): A ship that receives, stores, and converts LNG back into its gaseous state, then delivers it to a land-based pipeline or gas network

Green Shipping Finance: Financial activities and investments specifically directed towards environmentally sustainable projects within the maritime sector

Greenhouse Gas (GHG): A gas in the atmosphere, like carbon dioxide (CO₂ ) and methane (CH₄), that absorbs and traps heat, contributing to warming the planet’s atmosphere and surface.

Liquefied Natural Gas (LNG): A fossil fuel primarily composed of methane

LNG Bunkering Facility: Specialized systems, storage, and transportation facilities needed to safely supply LNG as fuel to ships

LNG-Fueled Vessel: A ship designed to run on LNG as fuel

LNG-Carrier Vessel (or LNG Carriers): A tanker ship designed to transport LNG as cargo

Loan: An agreement where a lender provides a sum of money to a borrower, who then promises to repay the borrowed amount (the principal) plus an additional cost (interest) over a set period under agreed terms

Multilateral Development Bank (MDB): International banks funded by multiple countries to support development projects worldwide

Public Finance Institution (PFI): A finance institution owned in majority by governments. Their main mission is to finance public policy — especially public investment — which can be broadly understood as spending aiming at building or preserving social or collective capital, whether material or immaterial, including environmental assets

-

In the maritime sector, fossil liquefied natural gas (LNG) has been touted as a transitional fuel under the assumption that it can help reduce greenhouse gas emissions (GHG) from the shipping industry — particularly CO₂ — in the short to medium term while infrastructure and technologies for cleaner alternatives are developed and scaled up.

However, fossil LNG is primarily composed of methane, a GHG that has a short atmospheric lifetime but is over 80 times more potent than CO₂. Methane emissions from ships fueled by LNG increased 180% between 2016 and 2023 (ICCT, 2025), with significant economic implications. The global LNG-fueled fleet’s estimated 247,000 tons of methane emissions in 2023 translated to nearly USD 950 million in annual climate damages—nearly four times higher than in 2016 (USD 250 million). This estimate builds on the U.S. Environmental Protection Agency’s (EPA’s) Social Cost of Methane, a monetary benchmark consistent with internationally recognized values, by incorporating the effects of ground-level ozone, a critical pollutant formed by methane (McDuffie et al., 2023). This figure still understates total harm, excluding other GHGs such as CO₂ and nitrogen oxides, localized air quality, and non-fatal health outcomes such as asthma and hospitalizations.

The science and policy landscape is challenging the business case for investment in LNG in the maritime sector. The latest IPCC report indicates that, to limit warming to 1.5°C, methane emissions must be reduced by a third by 2030 and almost halved by 2050 (IPCC, 2023). In 2023, the International Maritime Organization (IMO), in addressing the mid-term measures to reduce greenhouse gases, included the consideration and analysis of methane emissions in the sector (IMO, 2023). Additionally, 159 countries have signed onto the Global Methane Pledge, committing to take voluntary actions to contribute to reducing global methane emissions at least 30 percent from 2020 levels by 2030.

As these policies aligned with the Paris Agreement continue to shape shipping decarbonization, an LNG-fueled fleet would have no way to compete against zero-emissions shipping. Policy incentives to phase out the use of fossil fuels position fossil LNG shipping at a higher risk of stranded value during this transition (Fricaudet et al. 2022).

Financial institutions—including banks, insurers, asset managers, and development banks—manage significant capital and can guide investments towards a just and equitable transition to a decarbonized maritime sector. Despite commitments to decarbonization and net-zero policies, these institutions continue to invest in fossil LNG. Both private and public institutions are heavily funding maritime LNG projects through government-run schemes, directives and export credit agencies such as the European Union’s directive on the deployment of alternative fuels infrastructure, the European Investment Bank and the Japanese and Korean Export Credit Agencies (Fricaudet et al. 2022; Stand.Earth 2024), and earlier national support mechanisms like Norway’s NOx Fund.

This study examines how public finance is contributing to maritime LNG projects globally. Public and commercial datasets were assessed to generate a database of deals involving public finance institutions contributing to maritime LNG projects.

-

Public finance institutions (PFIs) are owned in majority by governments. Their main mission is to finance public policy—especially public investment—which can be broadly understood as spending aimed at building or preserving social or collective capital, whether material or immaterial, including environmental assets (Cingolani, 2019). In practice, however, PFIs have played a pivotal role in enabling fossil-fuel development by absorbing risks that private financiers are unwilling to take on. Through loans, credit guarantees, and insurance, they mobilize significant co-financing, making many capital-intensive fossil-fuel projects viable when they would otherwise be too risky. For example, between 2020 and 2022 alone, at least USD 142 billion in international public finance was directed towards fossil fuel projects (FoE, 2024).

Government-backed financing not only reduces the risks faced by private investors but also helps stimulate private spending. Given that transitioning to a decarbonized maritime sector will require rapid and large-scale investment in sustainable renewable energy and energy efficiency technologies, PFIs are well-positioned to help close the financing gap and mobilize private capital.

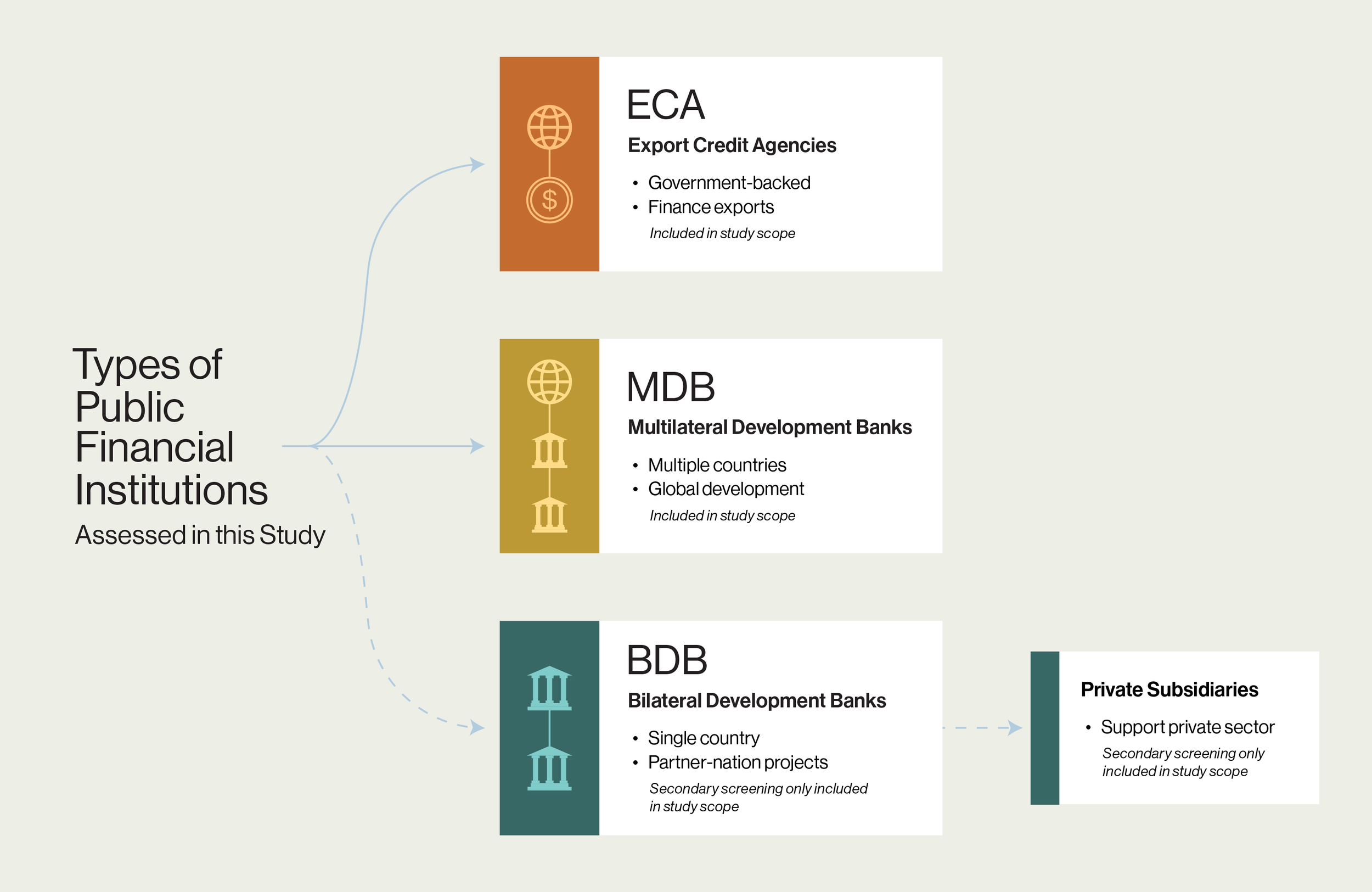

PFIs include multilateral development banks (MDBs), which are international banks funded by multiple countries to support development projects worldwide; export credit agencies (ECAs), which are government-backed institutions that fund export projects; and bilateral development banks (BDBs), which are funded by a single country to support projects in partner nations. The scope of this study focuses on MDBs and ECAs; BDBs were included in secondary screening, as well as their private subsidiaries (specialized arms that support private sector investment) (see Figure 1).

Figure 1. Study scope: Types of Public finance institutions (PFIs) assessed in this study to examine how public finance is contributing to maritime fossil LNG projects globally.

Maritime LNG projects include LNG bunkering infrastructure (the specialized systems, storage, and transportation facilities needed to safely supply LNG as fuel to ships), LNG carriers ( tanker ships designed to transport LNG as cargo), and LNG-fueled vessels (ships designed to run on LNG as fuel) (see Figure 2). While outside the scope of this analysis, the extraction, transport, processing, and storage of fossil LNG before it reaches a maritime LNG facility entails significant direct investment (IEA, 2024) and often overlooked social, safety, and geopolitical risks and costs (De Oliveira Menezes et al., 2025).

Figure 2. Study scope: Maritime LNG projects included in this study identified within the broader fossil LNG supply chain. This illustrates how maritime LNG has farther-reaching impacts—including extraction, transport, processing, and storage—beyond the study scope.

Approach

This research involves scoping public finance institutions involved in funding maritime LNG projects globally. Funding for maritime LNG projects that involved MDBs and ECAs were searched for systematically (by institution type and by name) using two global finance tracking databases: Marine Money and Public Finance for Energy. Tracking began in 2013, the earliest year for which public finance data was consistently available across both databases.

Funding for maritime LNG projects involving BDBs and their private subsidiaries was identified through secondary screening of MDB- and ECA-linked database records, but was not independently or systematically searched by institution name or type (see Appendix I). Resulting deals were compiled to generate a database of deals involving public finance institutions contributing to maritime LNG projects.

After completing the search, the database was reviewed for duplicate entries, and source links were re-checked to ensure accuracy. The database was then shared for external expert review. Reviewers suggested additional deals identified through similar searches in other subscription-based financial reporting websites. These deals were cross-checked against the inclusion criteria described above, and relevant ones were added to the database, noting when they could not be independently verified due to access restrictions.

The full scope of the search strategy and limitations with respect to the databases reviewed are described in Appendix I of the full report.

Results

USD 21.9 billion invested in maritime LNG projects

The resulting database tracks the total volume of unique institutional investments (deals) supporting maritime LNG projects. While the database incorporates commercial datasets that cannot be shared, the results here focus on institution- and country- specific deals. The search strategy identified 76 deals involving MDBs, ECAs, BDBs, and private subsidiaries of BDBs (see Table 1), supporting 62 unique maritime LNG projects, with total project investments reaching upwards of USD 21.9 billion (inconsistencies in financial reporting prevent the full verification of this projection; see Appendix I).

Of these, 21 deals were classified as supporting LNG bunkering facilities and/or LNG-fueled vessels. This category includes deals identified as including LNG bunkering infrastructure (5) and LNG-fueled vessels (16). More than half of the total investment — over USD 12 billion — was directed toward LNG-fueled vessels and bunkering infrastructure.

To put this allocation into perspective, USD 12 billion could instead support the electrification of approximately 480 small containerships, assuming costs comparable to the fully electric, zero-emission Yara Birkeland (120 TEU) (Morris, 2017). This comparison highlights the scale of public finance currently supporting fossil LNG infrastructure relative to investment needs for zero-emission shipping solutions.

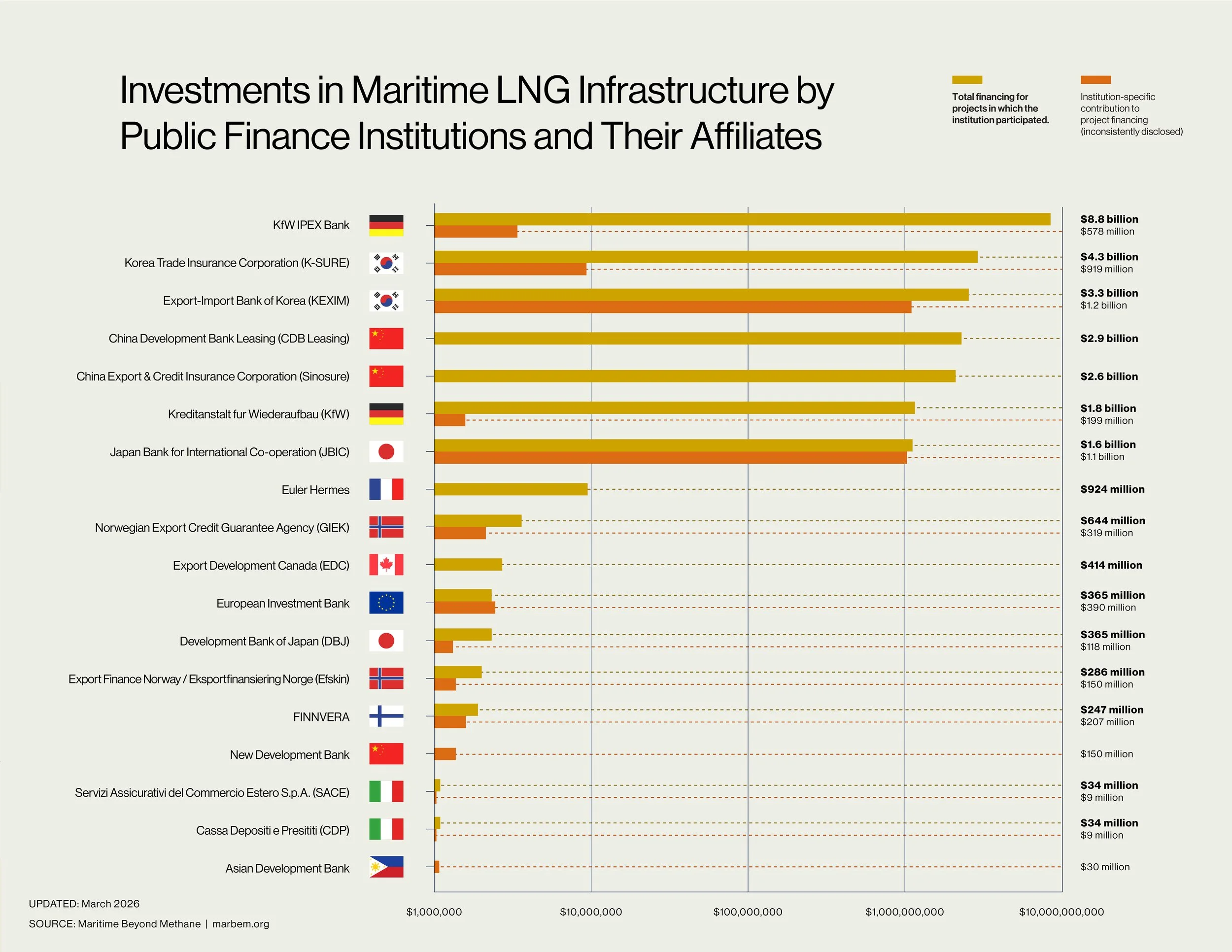

Figure 3. Investments (USD) in maritime LNG infrastructure by public finance institutions and their affiliates. Yellow lines indicate the total project financing associated with an institution, while orange lines indicate the amount specifically attributed to that institution’s contribution. Projects financed by multiple institutions are attributed separately to each contributor; therefore, aggregated totals exceed the value of unique projects. The two value types are not mutually exclusive: some projects report both total project financing and institution-specific contributions, while others disclose only one.